ESMA Unveils New Rules for Research – In mid-December ESMA (European Securities and Markets Authority) issued the long-anticipated final draft of its new regulatory framework, the Markets in Financial Instruments Directive II (MiFID II).

Institutional Investor magazine provided an update on January 15, 2015 on how MiFID II might handle payments for research and Corporate Access.

Some extracts from the piece:

Specifically, ESMA calls on the sell side to separate research payments from execution fees. For the buy side, research budgets must be established in advance and made plain to clients, with each agreeing to its share of the expense before the budget is implemented.

“That will be good for the ultimate investor, but it’s probably not good over the long haul for the big sell-side firms.”

The bulge brackets’ losses, however, could be independent providers’ gains. Michael Mayhew, chairman of Integrity Research Associates: “If I’m paying this large sell-side firm $1 million for research, and that same amount will get me ten different independent firms’ research, I’m probably going to have to reconsider my budget allocations. European asset managers will likely start reducing their dependence on the large sell-side firms and increasing their reliance on independent research.”

The U.K. regulator has already banned using commissions to pay for Corporate Access, judging management introductions to be outside the realm of substantive, proprietary research. In many ways, the MiFID II draft surpasses the FCA’s strictures.

“ESMA goes further in respect of saying the buy side must have a separate payment account for all research and advisory payments, with budget approval via clients, and even clearer separation from any trading commission spending,” Kelly explains. “ESMA is also more explicit in the need for transparent pricing of research services.”

The FCA requires “hard dollars for organizing and logistics of a road show, say, but permits commissions for the analysis and reports from an analyst that go alongside it.” ESMA’s proposed regulations, however, refers to certain “minor nonmonetary benefits” that the sell side can provide without separate billing, such as conferences and seminars. “This means ESMA is saying that parts of what the FCA would define as corporate access are okay to use commissions to pay for — or at least that is how I read it,” he says. “In this regard, ESMA is going less far, as it were, than the FCA, although personally I think it less likely the FCA will change its stance on corporate access.”

The real devil will be in the details to come, for the draft doesn’t tell market participants how to implement its directives. An open hearing is scheduled for February 19 in Paris, and public comments are welcome through March 2. Then, ESMA will finalize its recommendations and send them to the European Commission for approval before year-end. The new regulations will take effect at the start of 2017.

For the full article click here.

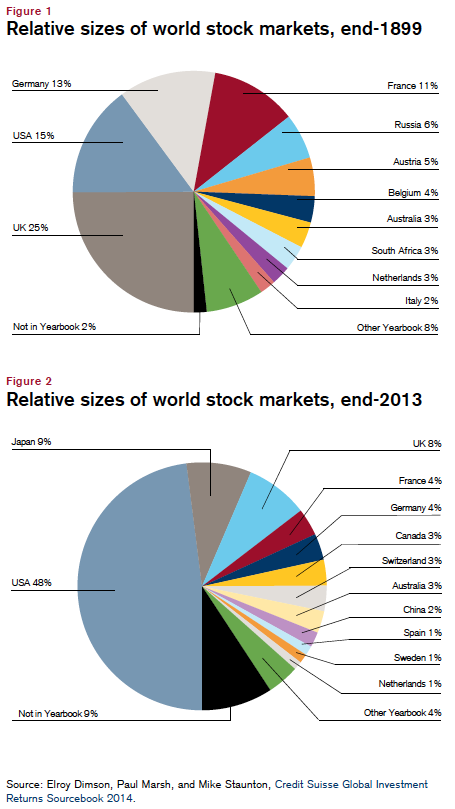

Europe’s 600 biggest companies (the Stoxx600) are less than half the size of the S&P 500.

Europe’s 600 biggest companies (the Stoxx600) are less than half the size of the S&P 500.